Volume 3: Supp-lie, Supp-lie, Supp-lie - The truth behind the Government’s housing affordability claims

This article asks a pretty simple question: if the Government’s housing plan is really about affordability, why does almost every lever make life easier for developers and investors? It looks at the evidence behind the “just build more” story and argues that market supply alone won’t fix a housing system shaped by land values, investor demand, tax settings, construction costs and developer profit margins. More homes are needed, but not like this. Affordability has to be built into the system, not wished for at the end.

Fair Growth Thornbury

5/4/202640 min read

We have a housing affordability crisis. That much is not up for debate.

In Melbourne, median house prices remain stubbornly out of reach for many, rents are sitting at or near record highs, and secure housing is becoming increasingly difficult to find. At the same time, Victoria’s public housing waitlist has reportedly grown to more than 65,000 people. That figure alone should give any government pause.

So, let’s start with something we can all agree on: Victoria (much like the rest of Australia and its allies) does not have enough affordable housing.

The real question is what we do about it.

If you listen to the Victorian Government, the answer is simple, almost suspiciously so. Build more market priced homes, build them faster, and affordability will follow. Across planning reforms, housing strategies, and public commentary, the message is remarkably consistent. Increase market supply and the rest will take care of itself.

This position has been heavily reinforced by a small but influential group of policy voices, most notably the Grattan Institute and the YIMBY movement. Their work is frequently cited to justify a market supply-led approach through zoning reform.

That framing is often presented as progressive, but it deserves a closer look. Many of its most prominent advocates are economists and policy commentators rather than planners, builders, urban designers or people with direct experience delivering housing on the ground. That shows in the way a deeply complex system is reduced to a simple supply curve.

And once you strip it back, the politics becomes clearer. The focus is not really on directly delivering affordability, but on deregulating planning, expanding private development capacity and letting the market run. Community input is recast as obstruction, public interest as inefficiency, and anything that sits in the way of development yield is treated as a problem to be removed. It is, at its core, a form of market liberalism presented as reform, asking a hypercharged version of the same system that created the crisis to somehow fix it.

Despite this, Labor Governments at both Federal and State level around Australia have latched onto this as the foundation of their housing policies. Boiled down, the Government’s housing agenda rests on three core assumptions:

A lack of housing supply is the problem, and increasing supply is the solution

Planning laws and local councils are the primary barriers to delivering that supply

Market-priced housing, delivered by the private sector, will ultimately solve affordability

The Premier captured this neatly in a recent statement: “The only way to make housing fairer for young Victorians is to build more homes, faster.”

It is a compelling line. It is also a very convenient one. Because once you move beyond the slogans and look at the broader body of evidence, the picture becomes far less certain. Many economists, housing researchers, and urban policy experts do not support such a singular view, particularly those not aligned to a single policy position.

When you interrogate these assumptions properly, each of them starts to unravel. And that is where things get interesting. If these assumptions do not hold, then the Government’s housing agenda is not just incomplete. It is misdirected.

At best, it risks delivering large volumes of housing that remain unaffordable to the people who need it most. At worst, it entrenches a system where housing outcomes are increasingly shaped by developers, investors, and financial institutions, while government continues to point to headline supply numbers as evidence of progress.

In other words, we get the appearance of action without the outcome that actually matters. Which raises a more uncomfortable question:

Is this really a plan to solve housing affordability, or simply a plan that looks like one?

Basic economics

If the Government were operating at a Year 10 economics level, you can understand how it arrived here.

One of the first concepts students learn is supply and demand. When supply exceeds demand, prices fall as sellers compete to secure buyers. When demand exceeds supply, prices rise. This is often illustrated with a fictional product. Economists love a good “widget.” If more people want widgets and supply does not keep up, the price increases. If you build more widgets, the price stabilises and eventually starts to fall.

Simple. Clean. Internally consistent. And, in the right context, completely correct.

There is no doubt Victoria has a growing population. As at 30 June 2025, the population sits just over 7 million, with projections pushing beyond 10 million by 2050. More people means more households, and more households means more homes.

So, the Government, backed by its preferred policy voices such as the Grattan Institute, has looked at this and reached what appears to be an obvious conclusion. We need more widgets. In this case, housing. The problem is that housing is not a widget. And treating it like one leads to very predictable mistakes.

Housing is not a uniform product

Not all housing is the same, and not all housing is equally in demand.

We are already seeing this play out. In many of the areas being heavily upzoned for apartments, developers are struggling to sell stock profitably. In some cases, apartments are being sold at a loss. Even the Grattan Institute has acknowledged softer demand for apartments in middle and outer activity centres. At the same time, Melbourne has more than 8,000 unsold apartments built since 2020. If supply alone were the issue, that stock would not be sitting there.

What this tells us is relatively simple. Building more homes is not enough. You need to build the right homes, in the right locations, for people who actually want to live in them.

Policy settings shape demand

This is where Australia’s policy settings start to distort the picture.

If housing were treated primarily as shelter, a place to live and build a life, then a supply-led model might carry more weight. Owner-occupiers would drive demand and the market might respond by delivering housing that meets their needs.

We have seen glimpses of this in practice. Across parts of Melbourne’s middle suburbs, traditional blocks have been redeveloped into four, five or six townhouses. That is a six-fold increase in density, delivered organically in response to demand. But that is not the full story.

Australia’s tax and policy settings treat housing more as a financial asset as opposed to homes for people to live. Negative gearing, capital gains concessions, and relatively permissive settings for investment, including foreign capital, mean that a significant portion of demand is not driven by people looking for a home. It is driven by people looking for a place to store and grow capital.

When that happens, the type of housing delivered shifts. It is no longer about what households need. It is about what sells to investors. That is one of the reasons why increasing supply does not automatically translate into affordability for residents.

Housing is not built on need alone

A critical point that is often missed in this debate is how housing is actually delivered.

Housing is not produced simply because people need somewhere to live. It is produced when projects are financially viable. Developers do not build to meet abstract demand. They build when buyers can secure finance at a level that covers land, construction, financing and risk, while still delivering an acceptable return.

That distinction, between underlying need and effective demand, is fundamental. It explains why periods of strong population growth do not automatically translate into equivalent increases in housing construction. More people needing homes does not mean more homes will be built, unless those people can participate in the market at the price required to make projects stack up.

This is not a theoretical issue. It is visible across the system.

Approved projects sit dormant for years. Sites change hands multiple times without development occurring. Schemes are abandoned after planning approval when costs shift or market conditions change. Feasibility moves, and projects disappear before construction even begins.

There is a price floor

There is also a more fundamental constraint that tends to get ignored.

New housing has a price floor. Developers will not build at a loss. At a minimum, sale prices must cover land acquisition, construction costs, financing, taxes, and a required profit margin. If those conditions are not met, projects do not proceed.

In Victoria, those costs are not trivial. Developer taxes are among the highest in the country. Labour supply is stretched, in part due to the demands of major infrastructure programs. Construction costs surged during COVID and have remained elevated.

Put those together and you get a simple outcome. It is extremely difficult to deliver new housing at genuinely affordable price points, regardless of how much supply you attempt to push through the system.

The data problem

Then there is the historical data.

Over the past decade, Australia has built housing at a faster rate than population growth. Population increased by approximately 15.9 percent, while the dwelling stock grew by around 19.4 percent. Over that same period, Melbourne’s median house price increased by roughly 96 percent. If supply alone were the determining factor, you would not expect to see that level of divergence.

This is where the simple supply narrative starts to break down. Population growth is not a perfect proxy for demand, particularly in a system where multiple buyers can compete for the same dwelling, and where ownership is not limited to those who intend to live in the property. The empirical evidence in Victoria over the past few years also seem to tell a very different story to the Government’s narrative.

The Government often points to Melbourne’s relatively softer price growth compared to other capital cities as proof that its supply-driven agenda is working. On the surface, that sounds plausible. It is also incomplete.

Because when you look at the underlying data, the link between that outcome and increased housing supply becomes difficult to sustain. Over the past two years, Melbourne has delivered fewer new dwellings than several other major capital cities. That is not what you would expect to see if a surge in supply, driven by planning reform, were the primary force moderating prices.

At the same time, development activity has been constrained. Fewer projects have commenced construction, and feasibility pressures across the sector remain well documented. So if supply has not meaningfully surged, what explains Melbourne’s relative price performance? A more widely accepted explanation points to changes in investor behaviour.

Victoria has introduced higher land taxes and expanded their application, including to certain investment structures and apartments. At the same time, rising interest rates have materially increased the cost of holding property.

Together, these factors have made Melbourne a less attractive destination for some investors. That matters, because investors have been a significant source of demand in the housing market. When that demand softens, prices respond.

In real terms, Melbourne house prices have fallen from their COVID-era peaks once inflation is taken into account. This has occurred alongside reduced investor activity and a slowdown in new construction, which leads to a slightly awkward conclusion for the current policy narrative.

If prices are moderating in an environment where supply has not materially accelerated, but investor demand has softened, then it becomes difficult to argue that supply is doing the heavy lifting. At the very least, it suggests that supply is not the only lever. And possibly not the dominant one. It is almost as if the data is pointing to something more complex than a single-variable explanation.

The “planning is the problem” narrative

The next major claim is that planning, particularly at the council level, is the primary reason housing supply has not kept up.

In this version of events, local councils are cast as the villains. Obstructive, slow, and captured by “NIMBY” sentiment, they are supposedly holding back developers who are otherwise ready and willing to deliver the housing Victoria needs. But this is also very difficult to reconcile with the data.

At the end of last year, the Municipal Association of Victoria reported that permits had been approved for more than 100,000 dwellings across Victoria that had not progressed beyond approval. To put that into perspective, Victoria’s public housing waitlist is estimated to be at least 65,000 people. So the question becomes unavoidable: If planning is the primary constraint, why are so many approved homes not being built? The answer is not particularly mysterious. It is viability.

Projects proceed when they make economic sense. When they do not, they sit. Or they are abandoned entirely.That is not a moral failing. It is how markets operate. Developers are not charities. They do not build homes out of civic duty. They build when the numbers stack up and importantly, this is not just a Victorian phenomenon. The evidence from Sydney is even clearer.

Research by Professor Bill Randolph at UNSW’s City Futures Research Centre shows that planning approval accounts for only around 15% of the total development timeline, from land acquisition through to completion. The majority of the process is dominated by financing, pre-sales, and construction. We also know that more than 95% of development applications are approved. In other words, the system is already saying “yes”.

And yet, like Melbourne, more than 100,000 approved dwellings in New South Wales are currently sitting unbuilt. Not blocked by councils. Not caught in red tape. Simply not viable in current market conditions. The planning system approved them but the market did not build them. This brings us back to the core issue, if a project cannot deliver an acceptable return once land, construction, financing, taxes and risk are taken into account, it does not proceed.

We have seen this across Victoria over recent years. Construction costs have increased, financing has tightened, and a number of building firms have become insolvent. Even projects with permits in hand have stalled and this is where the “planning is the problem” narrative starts to collapse entirely.Because even at a macro level, the drivers of housing prices sit elsewhere.

The Reserve Bank’s own modelling found that a 1% drop in interest rates can increase house prices by around 30%, while a 1% increase in housing supply reduces prices by just 2.5%. Given that new supply typically adds only around 1% to total housing stock each year, the arithmetic simply does not support the idea that planning reform alone can meaningfully move prices.

Those outcomes are driven by macroeconomic demand factors that sit well outside the control of local planning systems and authorities.

Even if councils were the problem…

But let’s give the Government the benefit of the doubt. Let’s assume councils really are the main problem. Let’s assume planning barriers are removed, zoning is liberalised, and developers are given broad freedom to build. Would that, on its own, deliver affordability?

This is where the Government’s position becomes even harder to defend (if that's at all possible). Because even in a world of mass upzoning, the same basic economics still apply. Projects need to be viable. Prices need to cover costs. Developers need margins. Investors need returns. And the market will prioritise the housing that generates the strongest return, not necessarily the housing that families need or ordinary people can afford.

Which means that more supply does not automatically translate into more affordable supply. That is the gap the current narrative struggles to close.

The homes we already have… but don’t use

But before we talk about building hundreds of thousands of new homes, it is worth asking a more basic question. How efficiently are we using the homes we already have? Because one of the more uncomfortable features of Australia’s housing system is that a meaningful portion of existing housing stock is not being fully utilised.

Research by Prosper Australia, using water consumption data across metropolitan Melbourne, found that in 2023:

27,408 dwellings recorded zero water use across an entire year, indicating they were likely completely vacant

A further 70,453 dwellings showed extremely low water use, suggesting they were only intermittently occupied

In total, close to 100,000 homes were either empty or underused across the city

Even allowing for debate about methodology, the scale is difficult to ignore (and it aligns pretty closely to census data from 2021).

To put that into perspective, that volume of housing is significantly more than the number of households currently on Victoria’s social housing waiting list. That should at least prompt a pause, because if housing were purely a supply problem, you would not expect to see tens of thousands of dwellings sitting idle while demand for secure housing remains so high. The explanation, again, comes back to incentives.

In Australia, housing is not just a place to live. It is a store of wealth. A financial asset. In some cases, a speculative one. Properties can be held vacant, used occasionally, or kept off the long-term rental market with relatively limited financial consequences. For some owners, particularly those with significant capital, the cost of leaving a property empty is outweighed by expected capital gains. From a market perspective, that behaviour is entirely rational but from a housing system perspective, it is deeply inefficient.

It also reinforces a broader point. Demand in the housing market is not simply driven by people needing somewhere to live.

To its credit, the Victorian Government has introduced a vacant residential land tax. But in its current form, it is unlikely to materially change behaviour. The regime relies heavily on self-reporting. Enforcement is an after thought (if at all). And the financial impost, relative to the value of the underlying asset, remains modest for many property owners.

In practical terms, it is a small signal. Not a structural intervention. So we are left in a position where housing, a scarce and essential resource, can be held out of circulation with relatively limited consequence. No meaningful requirement to make it available, no significant cost for not doing so and no direct pathway to connect that underutilised stock with the people who need housing most.

If existing housing is not being efficiently used, and if a portion of supply can be withheld or repurposed as an investment vehicle, then simply increasing supply does not guarantee better outcomes. It may increase the number of dwellings. It does not necessarily increase access or a pathway to safe and secure housing for all Australians.

What the evidence and experts say

Across the housing and planning literature, there is a consistent theme. Increasing market-rate housing supply, in isolation, does not reliably deliver affordability, particularly for lower and middle-income households.

Professor Christian Nygaard from UNSW’s City Futures Research Centre has noted that increasing supply may have marginal impacts, but it does not address affordability as a broader societal or wellbeing issue.

Dr Kate Shaw from the University of Melbourne is more direct stating that increasing density or market-rate supply alone will not meaningfully reduce prices.

Professor Nicole Gurran from the University of Sydney has observed that even during periods of significant construction activity, shortages of affordable housing have continued to grow.

Economist Matt Grudnoff has also highlighted that house prices have surged during periods when housing construction has outpaced population growth.

Taken together, these observations point to a consistent conclusion. The assumption that increasing market supply will, on its own, deliver affordability does not hold up particularly well under scrutiny. As Rachel Gallagher, lecturer in property development at Griffith University, has put it:

“The only durable solution is supply, but not market supply…”

Even without finishing the sentence, the implication is clear. The type of supply matters. If market supply alone were capable of delivering affordability, we would expect to have seen meaningful improvements by now. Instead, we have seen the opposite. More construction. More density. And housing that remains out of reach for many Victorians. And the consequences are not just economic.

As Michael Buxton, Emeritus Professor at RMIT, has consistently warned, planning reforms that prioritise rapid, market-led development risk reshaping cities in ways that undermine liveability, without delivering the affordability outcomes used to justify them in the first place.

Importantly, this is not just a theoretical or academic critique. There is a growing body of empirical evidence, both in Australia and internationally, examining what actually happens when governments pursue blanket upzoning and supply-led housing reforms. And the results are, at best, mixed.

In some cases, increased development has had limited impact on affordability. In others, it has contributed to rising land values, displacement of lower-income households, and a shift toward higher-priced housing stock. So rather than relying on assumptions about how the market should behave, it is worth looking at how it has behaved in practice.

That is where the gap between policy theory and real-world outcomes becomes much harder to ignore.

Example 1: Canada’s warning

Canada is a useful comparison because its housing debate has followed a very similar script to Australia’s.

Like Australia, Canada has increasingly treated housing as a financial asset, not just a place to live. Its policy debate has also been dominated by aggressive supply targets, planning reform, and incentives for private developers. As Kent Mundle argues in Next City, the deeper issue is the commodification of land. In his words, while governments can push for more construction, “new construction alone won’t make housing affordable” if urban land remains speculative.

That is why Vancouver and Toronto matter. They show what can happen when governments deliver the cranes, the towers and the developer uplift, but fail to deal with the underlying economics of housing. Vancouver, in particular, is one of the clearest warnings. For decades, it pursued a high-density, market-led development model. It got more housing. It got more density. It got the skyline. What it did not get was affordability.

Patrick Condon, a Canadian urban planner and academic, has argued that Vancouver’s experience exposes the limits of the supply-side story. Despite substantial densification, housing costs continued to detach from local incomes because the value of urban land, speculation and financialisation remained largely untouched.

Toronto tells a similar cautionary story. Canada’s current housing agenda has leaned heavily on supply-side targets and support for private development, while affordability remains constrained by land speculation and the financialisation of residential real estate.

The lesson is not that supply does not matter. It is that market-led density can deliver more buildings, more investor-oriented stock and higher land values without delivering affordability. In other words, they got the cranes. The people did not necessarily get the outcome they were promised.

Example 2: Chicago

Chicago provides a useful example because it shows how upzoning can affect land values before it delivers housing.

A study by Yonah Freemark examined Chicago zoning reforms in 2013 and 2015, which increased allowable density and reduced parking requirements near transit. The study compared property transaction prices and housing construction permits in upzoned areas against comparable areas that were not upzoned. It found significant increases in property values on parcels that received increased development capacity, but no statistically significant increase in housing construction in the short term. In plain English: the land became more valuable, but the housing did not arrive.

That matters because it goes directly to the risk with blanket upzoning. When government increases what can be built on a site, the market does not politely wait for affordable homes to appear. It prices in the uplift immediately. A block that could once support one home is suddenly valued as a development opportunity. That makes it more attractive to developers, investors and landholders, but less accessible to ordinary households trying to buy somewhere to live.

Freemark’s study does not prove that upzoning can never increase housing supply. It does show something more precise, and more relevant here: upzoning can increase land values without delivering meaningful new housing, at least in the short term. That is the affordability trap. The promise is more homes. The immediate effect can be more expensive land.

Example 3: New York City

New York gives us another important lesson: upzoning does not affect every neighbourhood in the same way.

A 2025 study by Kim and Lee examined neighbourhood-level upzoning in New York City and found that upzoning was associated with increased housing production, but also with rising prices and signs of gentrification.

In the long run, upzoned neighbourhoods became whiter, more educated and more affluent. The effects were also stronger where the upzoning was more intense, with those neighbourhoods experiencing greater housing production, stronger rent growth and higher housing price appreciation.

That is a crucial point. Even where upzoning produces more housing, it does not necessarily produce affordability. In some contexts, it can accelerate neighbourhood change in ways that benefit higher-income households while pushing lower-income residents further out. So again, the question is not simply: Did more homes get built? The better question is: Who were they built for, and who could still afford to stay?

Example 4: Brisbane

Brisbane may be the most directly relevant Australian warning.

A 2023 study by Cameron Murray and Mark Limb examined 19 upzoned areas in Brisbane over a 20-year period. Its title rather gives the game away: We Zoned for Density and Got Higher House Prices.

The study found that increased zoned capacity did not have the relationship with affordability that supply-side advocates often assume. Areas with more zoned capacity did not necessarily produce lower prices. Instead, rising prices appeared to be associated with rising new housing construction, even after controlling for zoning capacity.

That matters because it challenges the basic “planning story” underpinning the Government’s agenda: loosen zoning, get more housing, lower prices. Murray and Limb found a different pattern. Development appeared to occur where demand made projects viable, not simply where zoning allowed more homes to be built. In other words, the market did not obediently respond to planning permission by producing affordability. Rude of it, really.

Their conclusion is directly relevant to Victoria. While denser urban forms can bring benefits, zoning changes that support density should not be expected, by themselves, to deliver affordable housing. They argue that more direct interventions in urban land markets, non-market housing supply, and demand-side reform are likely to offer more promise.

That is the point the Victorian Government keeps trying to sidestep. Upzoning may change what can be built. It does not change what the market is designed to do.

Example 5: Fishermans Bend

Australia has other cautionary examples.

One of the problems with the “just upzone” argument is that it often treats land as if it is infinitely flexible. It is not. In cities like Melbourne and Sydney, well-located land is expensive because it is scarce. That scarcity does not disappear because planning controls are relaxed. In some cases, relaxing those controls can make the land even more valuable.

Fishermans Bend is a useful example.

The precinct was rezoned to allow large-scale residential development, with very generous development potential. Instead of producing an immediate wave of affordable housing, the rezoning reportedly caused land values in the area to double. The reason is not complicated. Once land can support significantly more dwellings, the market prices in that future development potential. Again, the uplift comes first. The affordable homes do not necessarily follow.

Fishermans Bend also shows another problem with supply-led planning. Development has been constrained by the absence of supporting infrastructure, particularly public transport. That makes sense. Developers may want the uplift, but they still need the project to be commercially viable and attractive to buyers.

But here is the trap. If the Government later delivers the infrastructure needed to unlock development, that public investment may further increase private land values.

So the public pays for the infrastructure. Landowners receive the uplift. Developers wait for the numbers to work. And affordability remains somewhere off in the distance, waving politely from a press release.

That is not a recipe for affordable housing. It is a recipe for publicly enabled private gain, unless the uplift is captured and directed back into genuinely affordable housing and infrastructure.

Example 6: Sydney

Sydney provides one of the clearest Australian examples of how upzoning affects land markets.

A 2025 study of three upzoned precincts in Sydney (Epping, Castle Hill and St Leonards) found that rezoning triggered sharp increases in land values and sales activity, in some cases far outpacing broader market trends.

The mechanism is important. Upzoning increases development potential, which increases land value. It also encourages land assembly, where owners combine and sell sites to developers, often at a premium. As one participant put it, it was “like winning the lottery but without buying a lottery ticket.”

The study does not suggest that upzoning inevitably leads to higher housing prices in the long term. It does show that, in the short to medium term, planning changes can significantly increase land values and reshape local markets.

And this is where the policy question becomes critical. If upzoning creates substantial private windfalls through increased land value, but governments rely on the private market to deliver affordability, there is a clear gap. The authors point to this misalignment, noting the reliance on private development and the difficulty in translating planning intent into affordable housing outcomes.

Which raises the obvious question: If public planning decisions create value, why is so little of that value captured for public benefit? Mechanisms such as inclusionary zoning, value capture, and direct affordable housing requirements are designed to address exactly this issue. Without them, upzoning risks doing one thing very effectively: Increasing the value of land.

And this is why the Victorian Government’s Activity Centre Program is so concerning.

The Government is creating significant new development rights across established suburbs, but without any meaningful value capture mechanism built into the planning model. No mandatory affordable housing requirement. No inclusionary zoning. No clear mechanism to capture uplift for public infrastructure.

No guarantee that the value created by public planning decisions is returned to the public. That means the uplift created by rezoning is largely left to be captured privately by landowners, developers and investors.

So when the Government says upzoning will deliver affordability, the obvious question is: How? Because if the policy creates private windfalls but does not require affordable outcomes, then affordability is not a plan. It is a hope. And hope is not a housing policy.

Example 7: The YIMBYs’ shining light - Auckland

Auckland is often held up as the definitive proof that upzoning works. And to be fair, it is the strongest case.

In 2016, Auckland upzoned a significant proportion of its residential land. Construction increased, and some studies suggest rent growth was moderated relative to what it otherwise may have been. If the supply story is going to work anywhere, it should be here. But the more important question is not whether more homes were built, it is whether housing became affordable. On that measure, the answer is far less convincing.

Even at its recent low point, Auckland’s median house price remained around NZD $930,000–$950,000 in 2025, before rising again to over $1 million. That still places housing at roughly 12–13 times median household income, well above commonly accepted affordability benchmarks. In other words, even in the most cited example of successful upzoning: Housing did not become affordable.

There are also important reasons to be cautious about how Auckland’s price movements are interpreted. Price declines were not unique to Auckland. They occurred across New Zealand, driven in large part by rising interest rates, reduced borrowing capacity, and weaker demand conditions. Migration slowed, and economic conditions softened.

At the same time, the nature of housing being delivered changed. New dwellings were significantly smaller on average, meaning that part of the “affordability improvement” reflected a shift in what was being built, not necessarily a reduction in the cost of comparable housing. A smaller apartment is cheaper than a larger home, but that does not mean it is affordable in the way most households understand it.

And as demand conditions have shifted again, prices in Auckland have already begun to rise.

Which brings us back to the core issue, if upzoning were, on its own, a reliable solution to affordability, we would expect prices to continue trending downward as supply increased. That is not what we are seeing. Even in its strongest case, upzoning has not delivered affordable housing at scale. At best, it has moderated pressures under specific economic conditions. That is a very different claim from the one being made in the current policy debate.

The YIMBY fallback: “filtering”

Faced with growing evidence that market supply alone does not deliver affordability, advocates of upzoning often retreat to a secondary argument. Filtering.

In housing economics, filtering is the idea that new housing is initially occupied by higher-income households, and only over time “filters” down to lower-income households as it ages. In effect, affordability is not delivered directly. It is expected to emerge gradually as wealthier households move into newer housing and leave older stock behind. This is a central pillar of the argument that simply increasing supply will eventually solve affordability.

The problem is that the evidence shows this process is slow, uncertain, and often insufficient, particularly for lower-income households. Research from the University of California, Berkeley’s Institute of Governmental Studies examined the relationship between housing production, affordability and displacement. It found that while filtering may occur over time, it “can take generations” to materialise, and even then does not necessarily produce housing that is affordable to low-income households. The same research found that market-rate housing production is associated with higher housing cost burdens for low-income households, even where rents may fall in later decades.

And importantly, the Australian evidence points in the same direction. Research examining housing dynamics in cities like Sydney and Melbourne has found that filtering does not operate as a reliable pathway to affordability. Where it does occur, it tends to be uneven and easily disrupted, and critically, far too slow to offset the pace of rent and price growth in these markets.

Even proponents of filtering acknowledge its limits. Transport and planning researcher Todd Litman argues that filtering can improve affordability over time, but accepts that it “does not provide quick relief” for those with the greatest housing need.

And research from UC Berkeley reinforces the same point more directly: “Producing market-rate housing alone will not improve affordability for low-income households.”

That is a significant concession, because it highlights the core issue. Filtering is, at best, a long-term and indirect mechanism. It relies on time, favourable market conditions, and assumptions about how housing moves through the market.

But it also relies on something else. A steady and responsive pipeline of new housing that is attractive for higher income earners to want to move into. Firstly, in most cases, the type of housing stock attractive to higher income earners isn't apartments, which is the primary built form being championed by the Victorian Government through its planning reforms. Secondly, a steady construction pipeline is not how the system operates in practice and

Housing is not built simply because there is demand for it. It is built when projects are financially viable. Developers bring projects forward when they can secure financing, achieve pre-sales, and deliver a return that justifies the risk. Which means supply is not constant. It comes in waves, tied to market conditions.

Filtering, by contrast, assumes a smooth and continuous flow of new housing through the system. That assumption does not hold. So even in theory, filtering is fragile. And in practice, it is unreliable.

It does not provide immediate relief. It does not guarantee affordability. And it does not address the needs of those most affected by the housing crisis.

Which raises a more fundamental question. If even supporters of the supply-side approach accept that affordability ultimately depends on subsidies, public housing, or direct intervention, then why is so much policy weight placed on massive upzoning and market supply?

So who actually benefits?

If upzoning does not reliably deliver affordability, the obvious next question is: Who does benefit?

The most consistent answer, across both research and industry commentary, is that the immediate beneficiaries are landowners, developers and real estate investors. That is not controversial. It is how the system is designed to work. When planning controls are relaxed and development capacity increases, the value of land increases. That uplift creates new opportunities for those positioned to develop or invest.

As financial advisory firm Aprio notes, upzoning “creates opportunities for real estate developers,” with higher property values encouraging investment in areas that may not previously have been considered viable. Similarly, real estate investment platform Millionacres highlights that upzoning can open up “a wealth of development opportunities,” lowering barriers to entry and enabling investors to generate returns from newly developable land. And importantly, those gains can materialise quickly.

Research examining zoning changes in Chicago found that property values in upzoned areas increased almost immediately following approval, reflecting the market’s rapid pricing-in of future development potential (Freemark, 2020).

That is the mechanism. Public planning decisions create private value and that value is captured first by those who own or can acquire the land. There is also a broader pattern that has been observed in a number of cities. Tom Angotti and Sylvia Morse, in Zoned Out!, describe how upzoning can trigger waves of speculative activity, with developers and investors moving quickly to acquire sites in newly upzoned areas. This can place upward pressure on land values and contribute to displacement pressures in lower-income communities.

That dynamic has been particularly visible in parts of the United States, where rapid redevelopment has often coincided with demographic change and the displacement of lower-income residents. It is important not to overstate this effect or assume it plays out identically in every context, but the underlying incentives are consistent. Upzoning increases development potential. Development potential increases land value. And increased land value attracts capital.

So while the policy is framed as a response to housing need, its most immediate and reliable effect is to improve the economics of development. So, if the primary, immediate beneficiaries of upzoning are those who already own land or capital, and affordability is expected to follow later, indirectly and uncertainly, then the burden of proof sits with those claiming it will deliver for everyone else. Because so far, the evidence suggests otherwise.

Does upzoning actually reduce rents?

One of the more measured claims made by proponents of upzoning is not that it will dramatically reduce house prices, but that it will at least help moderate rents. There is some evidence in the literature to support that proposition, particularly over longer timeframes, but local data raises questions about how reliably that plays out in practice.

Take Preston. Preston is a designated pilot Activity Centre and has already experienced significant increases in density, particularly following the level crossing removal program and associated redevelopment. More than 45% of its housing stock is now medium or high density, with further development underway.

If the supply narrative holds, this is exactly the kind of area where we would expect to see meaningful rental moderation. Yet according to Victorian Government rental data, median rents in Preston increased by more than 16% in the two years to September 2025. By comparison, neighbouring Thornbury, which has a much higher proportion of older, lower-density housing, saw rents increase by around 10% over the same period.

That is not definitive proof that upzoning increases rents but it does challenge the assumption that increased density automatically delivers rental relief. It also points to a broader issue: Where rents or prices do stabilise in high-density areas, part of that effect may be driven by changes in the type of housing being delivered. Smaller dwellings are cheaper than larger ones. A one-bedroom apartment will generally rent for less than a three-bedroom house. But that does not necessarily mean housing has become more affordable in a meaningful sense, particularly for families or those seeking long-term housing stability.

So even where rental outcomes improve, the question remains: What kind of affordability is being delivered, and for whom? Is rent reduction enough?

Even if we accept that upzoning may help moderate rents in some contexts, there are still important limitations to relying on that as the primary affordability strategy.

First, it shifts the policy objective away from ownership. Home ownership has long been one of the most important forms of financial security in Australia. In a system where income support payments are relatively modest, owning a home significantly reduces cost-of-living pressures later in life. A housing model that primarily delivers rental outcomes, without improving pathways to ownership, risks entrenching long-term financial insecurity for future generations.

Second, it reinforces the concentration of housing ownership. If most new housing is delivered through the private market and held as investment assets, a larger share of the population becomes reliant on renting from those who own property. That dynamic is already visible, with increasing participation from institutional investors and large-scale capital in residential property markets.

Left unchecked, it risks entrenching a system where:

ownership is concentrated

renting becomes the default

and housing operates more as an income-generating asset than a place to live

That may be efficient from an investment perspective, but it raises legitimate questions about whether it delivers the kind of housing system most Australians expect.

Build-to-rent: affordability, or just a different investor model?

You can already see this dynamic emerging in the Government’s growing reliance on build-to-rent. Under this model, developers receive tax concessions and planning support to construct large-scale rental buildings, which must generally be held as rental stock for a minimum period before they can be sold or repurposed.

The theory is straightforward. More institutional investment. More rental supply. More stable and, in theory, more affordable housing. But there is a fundamental tension at the heart of this model, build-to-rent does not change who builds housing. It is still delivered by private developers, funded by institutional capital, and designed to generate returns over time. The policy may change the ownership structure but it does not change the underlying economics.

These buildings still need to:

cover land acquisition costs

absorb construction costs

deliver ongoing yields to investors

And those costs ultimately shape the rents that are charged.

Which raises a simple but important question. If the model is designed to attract capital and deliver returns, why would we expect it to consistently deliver affordability?

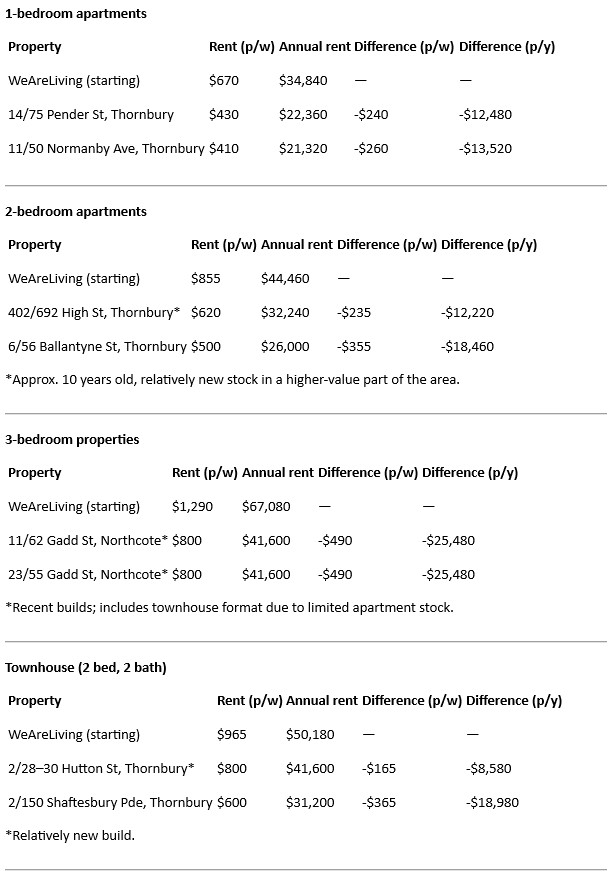

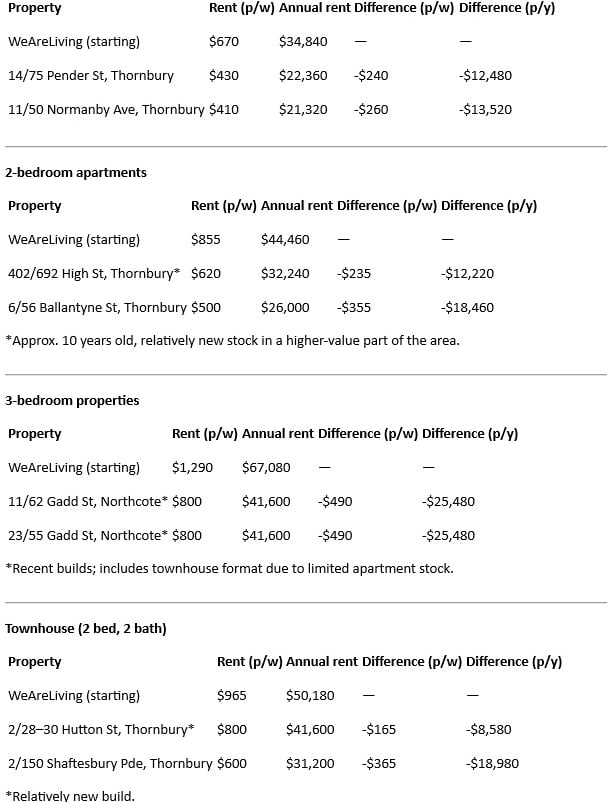

To test that, you do not need to look far. Again we look to Preston, one of the Government’s designated Activity Centre pilot areas, which has already seen significant densification, particularly following the level crossing removal program and associated redevelopment.

At the centre of that transformation is the Preston Junction build-to-rent development on the corner of High Street and Plenty Road. At approximately 18 storeys, it sits well above the surrounding built form and represents exactly the kind of project the current policy framework is designed to encourage: large-scale, high-density, investor-owned rental housing. It is also marketed accordingly.

The developer, WeAreLiving, describes the project as a reimagining of rental living, offering curated amenities, flexible lease terms, and a fully managed residential experience. In other words, this is not an edge case, it is the model. So if build-to-rent, combined with significant increases in height and density, is going to deliver affordability anywhere, it should be here.

What does this actually cost?

At the time of writing (23 March 2026), advertised starting rents at the Preston Junction build-to-rent development were as follows:

Studio - $545 p/w ($28,340 p/y)

1 bedroom - $670 p/w ($34,840 p/y)

2 bedroom- $855 p/w ($44,460 p/y)

3 bedroom - $1,290 p/w ($67,080 p/y)

Townhouse (2 bed, 2 bath) - $965 p/w ($50,180 p/y)

These are starting prices. Rents increase from there depending on layout, level, and availability.

To understand what this means in practice, we also looked at rental listings within the Activity Centre boundaries for older, existing housing stock, the type of housing that is likely to be replaced over time by developments of this kind. For consistency, we selected the most expensive comparable listings available at the time within the catchment.

How does it compare to existing housing?

In a word: Poorly. Across all property types it was significantly more expensive. Set out below is the outcome of our analysis:

Even when compared against higher-end existing stock, the gap is significant. Across the board, the new build-to-rent product is more expensive by:

$200 to $500 per week

or roughly $10,000 to $25,000 per year

That is not a marginal difference. It is the difference between being able to save or falling further behind. Between accessing housing or being priced out of it entirely.

If this is what “affordability through height” looks like, the problem is not that communities are sceptical. The problem is that they can read a rental listing.

What happens when “more homes” replace existing homes?

It is also important to understand how this new supply is actually delivered.

While the Preston Junction site itself was not residential prior to redevelopment, the Activity Centre Program is explicitly designed to encourage consolidation and redevelopment of existing housing stock across inner and outer catchments.That matters, because the sites most attractive to developers are not random.

They are typically:

larger blocks

older properties

and, critically, cheaper housing stock

In other words, the housing most likely to be demolished is often the housing that is already relatively more affordable.

So the question is not just how many homes are being built, it is also what is being lost in the process. If you demolish 10 or 12 older, more affordable homes and replace them with 80 or 100 new dwellings priced at a significantly higher level, you have increased supply, but you may have reduced the amount of affordable housing available.

Alphington: a local case study

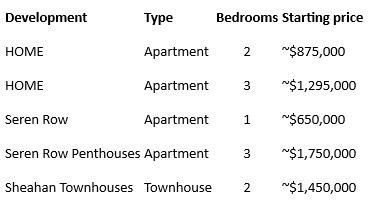

Just down the road, the redevelopment of the former Alphington Paper Mill site (YarraBend / HOME Alphington) provides a useful example. The project is delivering approximately 2,500 dwellings across a mix of apartments and townhouses, including a 16-storey tower and multiple medium-density developments.

On its face, this is exactly the kind of large-scale supply increase often cited as necessary to address the housing crisis but the composition of that supply tells a different story. According to council information, only around 5% of dwellings are designated as affordable housing. That is roughly 125 homes out of 2,500. The rest are market-rate properties.

And the pricing reflects that:

These are not outliers. They are typical of new development pricing in the current market. In fact, the new 'Thornbury House' development, granted additional height above the activity centre heights and fast tracked by the Planning Minister in exchange for a measly 3% affordability payment, shows what's actually on the way. The entry level 1 bedroom apartment without a car parking spot starts at a whopping $620,000. And on that extra 7th storey granted in exchange for the 'affordability' payment? A smaller $3,000,000 penthouse and the 'Colossal' penthouse that's so expensive, the price isn’t even listed.

Why this keeps happening

The answer lies in development economics. As stated previously, new housing must, at a minimum, cover:

land acquisition costs

construction costs

financing costs

and a developer margin

And the costs have increased significantly and developers are always going to be looking to maximise their margin. They simply will not build things that do not provide maximum profit for their investment.

As industry commentary has noted, rising construction and financing costs are limiting the ability to deliver new housing at lower price points, even where overall price growth has slowed. Developers respond accordingly. They do not build where it is not viable. They do not price below cost and increasingly, only higher-end developments are stacking up financially. As one planning consultant put it: “Developers just won’t develop if it means they won’t make money… only the high-end, luxury developments are stacking up financially at the moment.”

This creates a structural problem. New housing is more expensive to deliver than existing housing, which means it is typically priced above the existing market, not below it.

So when older, lower-cost housing is replaced with new, higher-cost housing, the outcome is not necessarily improved affordability. It is often the opposite. More homes. Higher prices. And a shrinking pool of genuinely affordable housing.

The “apartment-first” future

The Government’s approach also implies something broader about the future of housing. Even if the system does eventually deliver access to ownership, it increasingly assumes that for the next generation, that ownership will take the form of an apartment in a large-scale development.

That is not inherently a problem. Apartments play an important role in any growing city but it does raise important questions about how this model functions over time. Historically, home ownership in Australia has not just been about shelter. It has been a pathway. People would enter the market, build equity, and, over time, upgrade into different forms of housing as their needs changed. That pathway becomes less certain under an apartment-first model.

Partly because of supply dynamics. As more detached and family-oriented housing in established suburbs is redeveloped into higher-density formats, the relative scarcity of that housing type increases. That can place upward pressure on prices, making it harder for households to transition into those homes later. The result is a system where people may enter the market, but find it increasingly difficult to move within it.

There is also a separate, but related issue. The quality and long-term cost of new developments. Concerns about construction quality in large parts of the apartment sector are well documented, including issues relating to defects, remediation costs security design and building performance. These are not universal, but they are sufficiently common to affect market confidence and for buyers, that introduces additional risk.

Ownership costs can also be less predictable than they appear at the point of purchase. Ongoing costs such as owners corporation fees, maintenance obligations and building management expenses can increase over time, particularly once initial arrangements put in place by developers transition to full operational cost structures. None of this means apartments are inherently a poor form of housing but it does mean that they operate differently. And those differences matter when they become the primary pathway into home ownership.

All of this sits within a broader regulatory environment that is under strain. Planning reforms are being used to accelerate development and increase supply, but the success of that approach depends on the strength of the systems that sit around it:

building quality and compliance

consumer protections

governance of shared ownership structures

and the alignment of incentives across developers, managers and owners

If those systems are not robust, scaling up development carries risk for individual buyers and the long-term performance of the housing system itself. And the truth is, in Victoria, they are far from robust. The entire system is currently heavily weighted in favour of developers and the property industry players such as owners corporation managers, domestic building insurers (or the lack of legal requirements for such a policy to be held) and building inspectors, leaving owners stuck without a chair when the music stops after settlement.

This is the core tension in the current model. We are being asked to rely more heavily on:

higher-density housing

delivered faster

by private developers

in a system where long-term outcomes are not always well aligned

That may increase dwelling numbers but it does not automatically produce a housing system that is:

stable

affordable

or aligned with how people want to live over time

So what actually works? (And what isn’t being done)

If upzoning and market-led supply are not delivering affordability, the question becomes obvious: What actually does?

There is broad consensus across the housing literature that direct provision of affordable and social housing is the most effective way to address housing affordability for lower-income households.

But this is where the Victorian Government’s approach becomes difficult to reconcile. Rather than materially increasing public housing stock through direct investment, the Government has leaned heavily on public–private partnership models to redevelop existing public housing sites.

The pitch is familiar. Redevelop ageing public housing. Increase overall dwelling numbers. Deliver a “net increase” in social housing. But the detail tells a more complicated story.

Take a number of recent projects:

Walker Street, Northcote

87 social homes replaced with 250 total dwellings

→ 99 social homes (+12)

→ 151 market homesAbbotsford Street, North Melbourne

112 social homes replaced with 340+ dwellings

→ 127 social homes (+15)

→ ~200+ market dwellingsBrunswick West

82 social homes replaced

→ 119 social homes (+37)

→ 50 market homesOakover Road, Preston

→ 99 social homes

→ ~194 market homesAlphington (Nightingale partnership)

~70 homes delivered

→ 7 “affordable” homes (not social housing)33 Alfred Street, North Melbourne (planned)

~800 total homes

→ 300 social homes

→ ~500 non-social dwellings

The pattern is relatively consistent. There is usually a modest increase in social housing accompanied by a much larger increase in market housing on public land. This is not a neutral policy design, it reflects a deliberate model:

Public land is redeveloped

Private development is enabled at scale

Social housing increases slightly

Market housing increases significantly

The result is often framed as a success because total dwelling numbers increase but the critical question is not total supply, it is the composition of that supply. Because the housing crisis is not evenly distributed and it is most acute for those on lower incomes. For those groups, a small increase in social housing does not offset the scale of need.

That's not to say the Government is doing nothing on social housing, the issue is that what they are doing is nowhere near the scale required to actually combat the crisis we face. Instead they want to outsource it to a private sector that wants to build no affordable housing at all.

What the evidence says about this approach

Research into “social mix” and public–private redevelopment models raises further concerns.

As noted in evidence to parliamentary inquiries: Social mix policies “consistently fail to deliver improved outcomes for low-income tenants” and instead tend to benefit higher-income households while increasing risks of displacement and reduced housing stability.

Similarly: Public–private partnership models often result in poor returns to the public, permanent loss of public land capacity, and limited benefits for tenants.

These findings go directly to the heart of the current approach because they suggest that the model being used is not just insufficient. It may be structurally misaligned with the goal of delivering affordable housing.

This matters even more when viewed at a system level. Victoria has one of the lowest proportions of social housing in the country, at around 2.8–3% of total housing stock. That is well below comparable countries:

Netherlands: ~29%

Austria: ~24%

Denmark: ~21%

France: ~17%

UK: ~17%

New Zealand: ~5%

At the same time:

Around 34% of people seeking homelessness assistance in Victoria do not receive it

Growth in public housing stock has been extremely limited over the past decade (a decade during which the Victorian Labor Government has exclusively been in power)

In that context, marginal increases in social housing delivered through redevelopment projects are unlikely to meet the scale of demand. The Government is relying on:

private development

market supply

and indirect mechanisms

to solve a problem that is fundamentally about access to housing for those the market does not serve. And when it does directly intervene, it does so in a way that:

limits public investment

relies on private delivery

and increases market exposure on public land

If the objective is to deliver affordable housing, particularly for lower-income households, the evidence points in a clear direction. You need to build it. Directly. At scale. And with policy settings designed to prioritise affordability, not just total dwelling numbers.

Because without that, more homes does not mean more affordable homes and, in some cases, it can mean the opposite.

The mid-rise code: designed for delivery, not affordability

The Government’s mid-rise housing code is often presented as a key part of the solution. Standardise approvals. Reduce planning friction. Get more homes built, faster.

On its face, that sounds sensible, but when you look at the detail, a different picture starts to emerge.The code is not primarily designed to make housing more affordable. It is designed to make housing more deliverable for developers.

That distinction matters. Because many of the changes embedded in the code are about improving feasibility:

reduced setbacks

simplified design requirements

fewer constraints on building envelopes

more flexibility in site coverage

These changes lower development costs and increase yield. They make more projects stack up financially, but there is no corresponding mechanism that requires those savings to be passed on to buyers or renters.

The other side of that equation is design quality. To unlock feasibility, standards are relaxed. That means:

reduced access to natural light

increased overlooking and reduced privacy

smaller private open space

tighter building footprints

Individually, these may seem like marginal trade-offs, but scaled across thousands of dwellings, they fundamentally shape the quality of housing being delivered. And importantly, they shape who that housing is suitable for. Apartments with limited light, reduced privacy, and constrained space may function as short-term rentals or entry-level ownership, but they are far less suited to long-term living, particularly for families.

So the code:

reduces design standards

increases development yield

improves developer feasibility

but does not require affordability outcomes, which means the most likely result is more housing, built faster, at lower quality and at broadly the same price point the market can sustain. Because again, the price is not set by cost. It is set by what buyers and renters can afford to pay.

The risk is not just that affordability is not delivered. It is that we lock in a generation of housing that:

is smaller

performs worse

and may not meet long-term needs

while still being priced out of reach for many. That is not a housing solution, it is a trade-off where the benefits and costs are not evenly distributed.

When the evidence doesn’t fit, change the politics

So what happens when the premise is flawed, the evidence is contested, and the numbers do not support the slogan? You change the argument. That is what we are seeing now.

Rather than engaging seriously with the limits of market-led supply, the Government has increasingly relied on political tactics designed to narrow the debate. Communities are dismissed as selfish or anti-housing, younger people are told older residents are standing in their way, councils are blamed for a housing crisis driven by far broader market, tax, construction and investment dynamics.

Consultation is structured in ways that create the appearance of engagement, while key decisions, modelling and assumptions remain difficult to scrutinise. Dissent is not answered. It is branded as obstruction.

That is not evidence-based reform. It is political packaging.

Complex problems rarely have simple solutions. But simple solutions become very convenient when they align neatly with the interests of developers, investors and institutional capital. And that is the uncomfortable conclusion this Government does not want Victorians to reach.

This is not a serious plan to solve housing affordability.It is a plan to liberalise development, inflate land values, weaken standards, sideline communities and hope that affordability somehow appears at the end.

That is not housing policy. It is a sell-out dressed up as reform.

What would actually move the dial?

If the problem is structural, the solution has to be as well. That means moving beyond a narrow focus on supply and addressing how housing actually operates in Australia — as both shelter and a financial asset. Right now, policy leans too heavily toward the latter. A credible response needs to rebalance the system.

1. Treat housing as housing, not just an asset

Australia’s tax and investment settings play a major role in shaping housing demand.

At present, they incentivise:

holding property for capital growth

investing in existing stock

and treating housing as a wealth accumulation tool

Reform should focus on:

Capital gains tax (CGT) reform to reduce speculative incentives

Negative gearing reform, particularly to shift demand toward genuinely new supply

Targeting investment so it adds to housing stock rather than inflating the price of what already exists

The goal is not to remove investment, it is to align it with housing outcomes.

2. Capture public value through planning

When governments rezone land or increase density, they create significant value. Right now, much of that uplift is captured privately. That is a policy choice. Other jurisdictions take a different approach, using:

mandatory inclusionary zoning

affordable housing quotas tied to development approvals

value capture mechanisms linked to rezoning and infrastructure investment

Without these, planning reform risks doing one thing very effectively, increasing land values without delivering affordability.

3. Bring housing back into use

We also need to address the underutilisation of existing housing. A meaningful number of properties sit vacant or underused, reflecting the role of housing as a store of wealth rather than a place to live.

Policy responses should include:

stronger vacancy taxes, with real enforcement

measures targeting land banking and long-term vacancy

incentives to bring existing dwellings back into active use

Housing that exists but is not used is not solving the crisis.

4. Build what the market won’t

This is the most important lever. The market does not reliably deliver housing for lower-income households. That is not a failure. It is simply not what the market is designed to do.

So if affordability is the goal, particularly for those most affected, there is no substitute for:

direct investment in public and social housing

non-market housing models

delivery at scale, not at the margins

International evidence is clear. This is what works.

5. Build more homes — with communities, not against them

We do need more homes, but how we build them matters just as much as how many we build.

The current approach too often treats community input as a barrier, rather than a resource. That leads to blunt, one-size-fits-all outcomes that generate conflict and fail to deliver places people actually want to live.

A better approach means:

place-based planning, not blanket upzoning

alignment with infrastructure, so services arrive with growth

genuine community engagement, where input shapes outcomes

When done properly, this does not reduce supply, it improves it. Housing that fits the area, meets long-term needs and is delivered with community support. Because the real trade-off is not between more homes and liveability, it is between planning done well and planning done poorly.

None of this is radical. It is a recognition that housing policy is not just about how many homes are built. It is about:

who they are built for

how they are priced

and who benefits from the system

Until those questions are addressed directly, increasing supply alone will not resolve the affordability crisis.

Conclusion: The affordability lie

Victoria does not need another housing slogan. It needs a housing policy that is honest about the problem it claims to solve.

The Government’s story is simple enough: build more homes, build them faster, trust the market, and wait for affordability to arrive. But after everything we have seen, that is not a plan. It is a punt being made with our suburbs, our public land, our future housing system, and the lives and futures of the next generation.

The evidence does not support the idea that blanket upzoning, weaker standards and market-led development will deliver affordable homes at the scale required. What it does suggest is far more uncomfortable: land values will rise, developers will build when the numbers suit them, investors will capture returns, and older, cheaper housing will be replaced with newer, more expensive housing. Communities will then be told this is the unavoidable price of progress.

But progress for whom?

If the end result is more unaffordable apartments, higher land values, weaker liveability standards, and a generation pushed into renting for life or buying smaller homes in riskier developments, then we have not solved the housing crisis. We have redesigned it.

That is the lie at the heart of the current agenda. The Government says this is about young people, fairness and giving Victorians somewhere to live. But a policy that does not require affordability, does not capture public value, does not properly fund infrastructure, does not build public housing at scale, does not look at housing stock diversity and does not meaningfully listen to communities is not an affordability policy. It is a development policy.

Victoria can do better. We can build more homes without surrendering liveability. We can increase density without handing public value to private interests. We can plan for growth without treating communities as obstacles. And we can deliver affordable housing if we are prepared to actually build it, protect it and prioritise it.

The answer is not less ambition. It is more honesty, more courage and a housing system that starts from a simple proposition: homes are for people first, not portfolios, press conferences or developer margins.

Until that becomes the starting point, the affordability crisis will not be solved. It will simply be repackaged, rezoned and sold back to us at a higher price.

Contact

Get in touch:

© 2025. All rights reserved.

Fair Growth Thornbury acknowledges the Wurundjeri Woi-wurrung people of the Kulin Nation as the Traditional Custodians of the unceded lands on which we live and work. We pay our respects to Elders past, present and emerging.

Authorised by J Patto, Level 3, Suite 329/98-100 Elizabeth St VIC 3000